During the AI boom, investors have fixated on flashy chip designers and massive data-center builders. Yet the real AI enablers frequently sit one layer deeper — in the specialized materials that make high-speed optical connections possible.

As data centers demand ever-faster photonics to handle exploding AI workloads, companies supplying critical substrates like indium phosphide (InP) find themselves in the spotlight. The question that smart investors should ask: Can a small player like AXT (AXTI) turn this tailwind into sustainable gains, or is the surge pure hype?

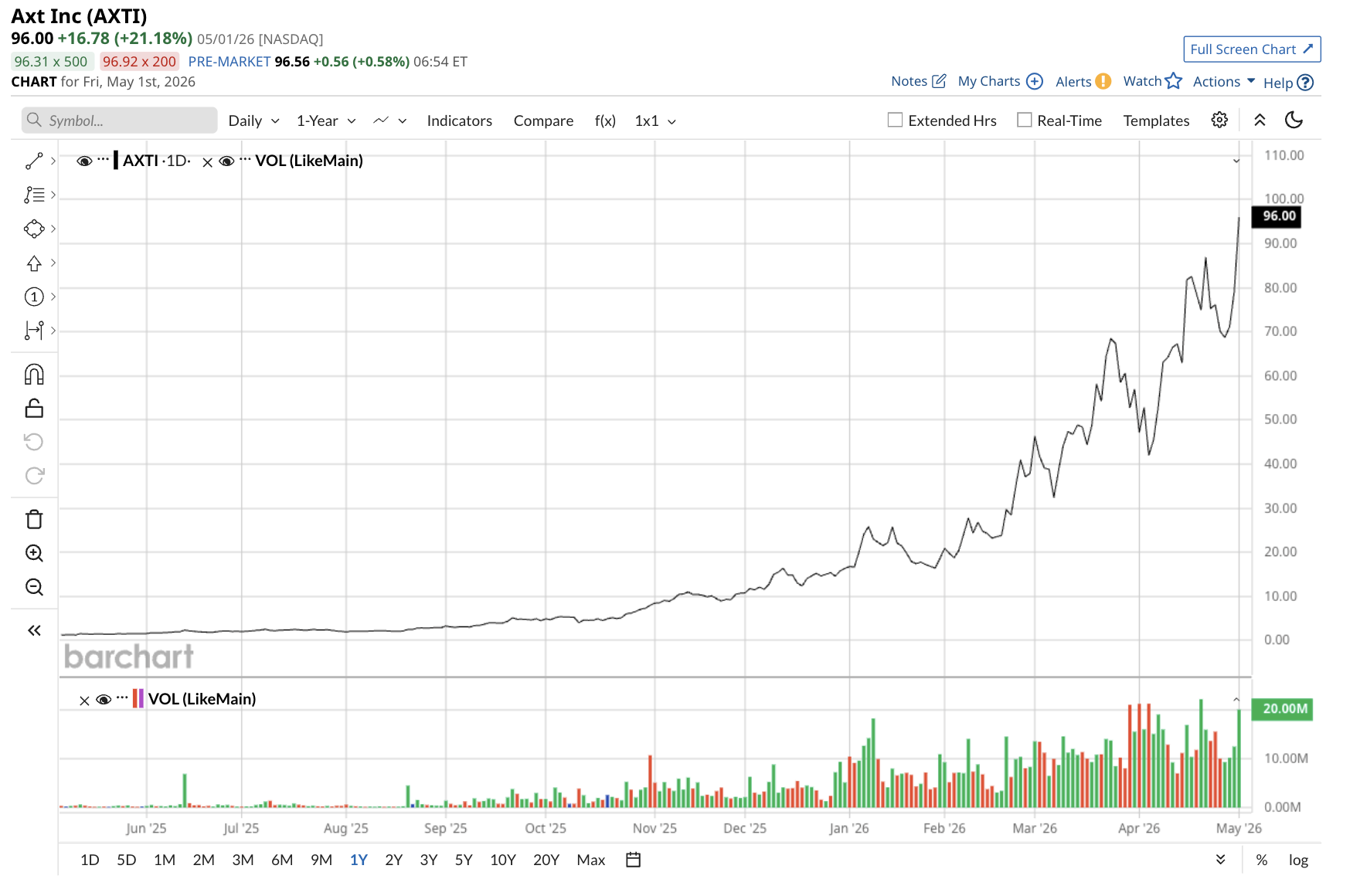

AXTI Stock's Stunning Performance

On a year-to-date (YTD) basis, AXTI stock has delivered a staggering 548% return, turning a modest starting position into nearly seven times its value. That dwarfs the S&P 500's ($SPX) approximately 6% gain over the same period. The semiconductor industry has seen strong performance, but AXTI stock has outpaced most peers by a wide margin.

Over the trailing 12 months, the stock has returned more than 7,900%, rising from a 52-week low near $1.23 to recent highs above $110 following a 21% gain on May 1 and a 10% gain on May 4. AXT is nearing profitability and guided the second quarter to positive EPS on AI-driven InP substrate demand. The stock's trajectory reflects investors betting that surging InP wafer demand will continue.

What Exactly Does AXT Bring to the Table?

AXT designs, develops, manufactures, and distributes high-performance compound semiconductor substrates, primarily indium phosphide, gallium arsenide, and germanium. These wafers serve as the foundation for lasers and detectors in high-speed optical networks — exactly what AI data centers need for faster, more efficient data movement.

In the company's recently relaeased Q1 report, AXT reported revenue of $26.9 million, up 39% from $19.4 million in the prior-year period and beating estimates of $26.7 million. Indium phosphide revenue reached $13.6 million, highlighting its growing role. The company also holds a substantial backlog, and management plans to expand InP capacity.

Valuation Snapshot

Traditional metrics show that AXTI stock trades at a premium. The price-to-sales (P/S) ratio stands at around 71.1 times, while the price-to-book ratio sits at 18.1 times with book value per share of around $5.37. Return on equity is negative at -6.1%, return on assets is around -3.8%, and profit margin is -24%. Trailing EPS comes in at roughly -$0.32, reflecting ongoing investments in growth.

That's a fancy way of saying the market prices in significant future expansion from AI photonics demand. With a market cap exceeding $6.9 billion, AXTI commands a valuation far above current revenue, betting that capacity ramps and margin improvements will eventually justify it. Compared to larger semiconductor material peers, it carries higher risk but also higher perceived upside from niche positioning.

Granted, challenges exist. The company remains unprofitable, with Q1 2026 GAAP net loss of $1.6 million (or $0.03 per share), although this figure narrowed from $8.8 million a year earlier. Gross margin improved to nearly 30%.

Manufacturing occurs mainly in China, exposing AXT to geopolitical tensions, export restrictions, and supply-chain volatility. Capital raises have also diluted shareholders to fund expansion. That said, sequential revenue growth and a strong backlog suggest execution is improving.

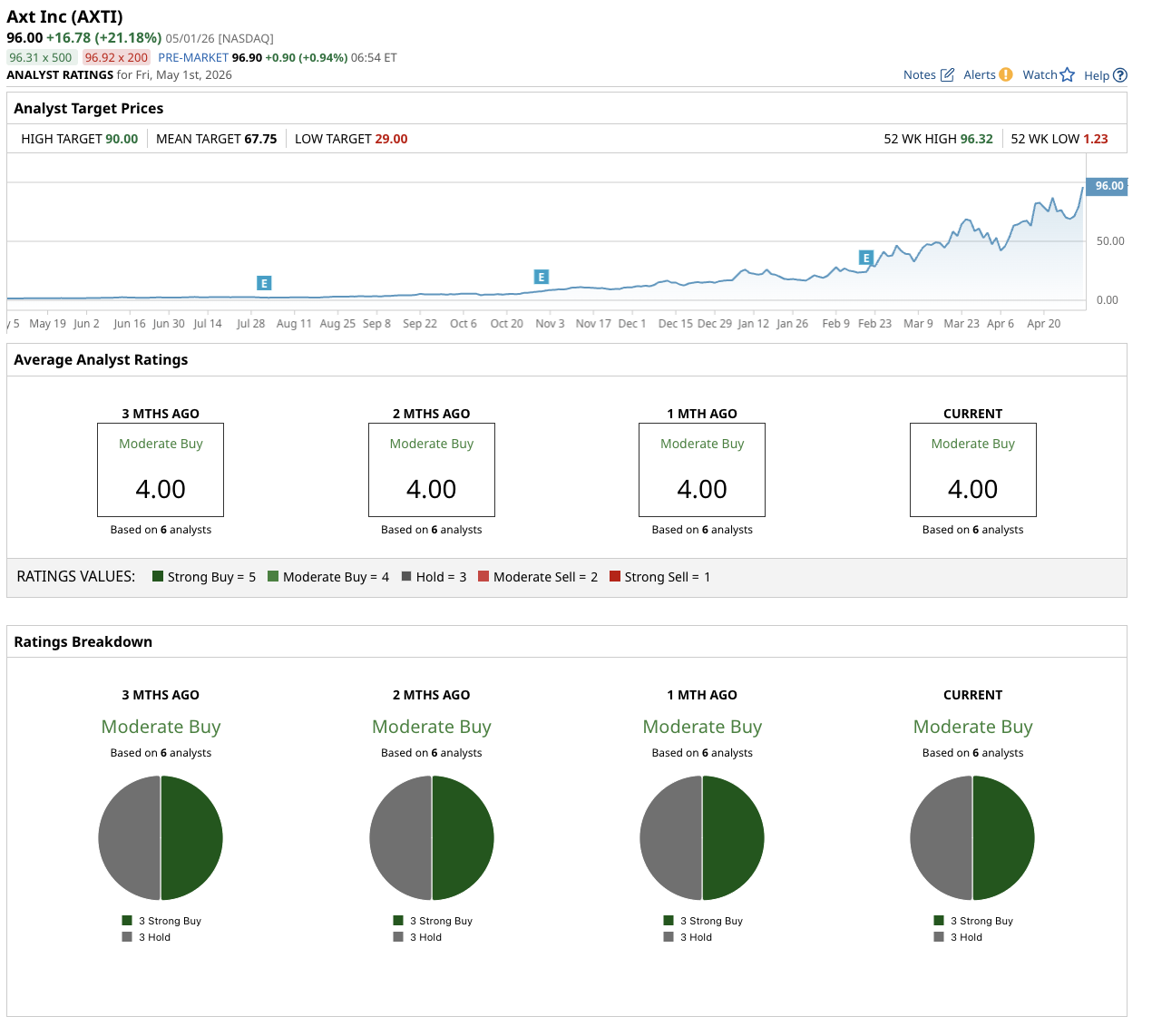

What Do Analysts Think About AXTI Stock?

Analysts maintain a consensus "Moderate Buy" rating on AXTI stock, based on six analysts split between three "Strong Buy" ratings and three "Hold" ratings. That consensus has held steady over recent months. The mean price target of $68 sits significantly below current levels, implying 36% potential downside from here, with a high target near $90 and a low target of $29. This highlights a wide gap between Street forecasts and market enthusiasm. Analysts appear more cautious than the share price suggests, focusing on execution risks amid the capacity buildout.

The Bottom Line

AXTI stock offers a high-conviction way to play the optical AI infrastructure buildout through its specialized substrates. The numbers show explosive YTD performance and improving fundamentals, but elevated valuation and profitability hurdles mean it suits risk-tolerant investors who can handle volatility.

Sharp investors should watch AXT's Q2 performance and whether it hits capacity milestones. Treat AXT as part of a diversified tech portfolio rather than a core holding. When all is said and done, material plays like this can deliver outsized rewards — provided the AI demand story stays on track.

On the date of publication, Rich Duprey did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.